Jerry had reached the bottom of the barrel when it came to credit. He wasn’t even trying to make it better, because he thought it was no use.

He had late payments, collections, and even a car repossession on his record. So he just accepted the fact that he had no credit and got along the best he could.

But then a few friends started encouraging him to try to get his credit scores rebuilt. After all, he was still a young man and someday he would want to buy a home. He might even want to own a car that was too expensive to buy with cash. He needed to get with building a new credit reputation.

So Jerry took their advice. The first step was to get a copy of his credit report with scores. He saw that the collections were nearing the 7 year mark, when they should automatically fall off his report.

They did, and when he saw the boost it gave his scores, he was encouraged. He got a “bad credit credit card” and began using it wisely, and after a few months he saw another little jump in his credit scores. Now he was cooking!

The next thing was to get another car loan. He was careful… he chose a low priced used car with a payment he knew he could afford, even though he was paying a pretty high rate of interest.

The next time he checked his credit scores he expected to see an even better number.

But… instead it was lower.

Jerry was in shock. Here he’d been working so hard to raise his credit scores and be a responsible consumer, and his scores just fell! What went wrong?

What went wrong was that Jerry had been moved to a different risk category.

Credit scoring models place each consumer in a risk category with others who have a similar credit history. Jerry started out in a category that included late payments, collections, and a car repossession. His scores were determined by comparing him to others with a similar history.

When those collections “aged out” of his credit report and he began using credit responsibly, his scores improved. But then, when he added the car loan and began making payments on time, he got moved to a “better” risk category, where he compared less favorably to others in his category. And… his scores decreased.

So, while most of us believe that all consumers are scored by the same standards, it isn’t so. We’re each scored by comparison to others in our risk category. And interestingly, a late payment will have less effect on a person in a high-risk category much less than it will on a person in a low-risk category. When low-risk consumers make a credit mistake, their scores tumble quickly.

Jerry got over his shock and kept working to improve his financial picture – and he’s well on his way to a place in a low-risk category. But seeing his scores drop when he was working hard to establish credit nearly caused him to give up the goal.

An attorney can be a life saver and at the same time they can cause havoc. I recently received a call today from someone wanting to buy a house. This individual, we will call him Bob, was advised by a judge back in 2009 to stop all payments on a house to force a short sale. This was all the result of a divorce. This may sound crazy, but the soon to be ex-wife did not want any part of the obligations involved with the property during this divorce. So the Judge forced a court ordered short sale on the home.

Bob was advised by the attorney that this process would not affect his credit. Well the part they forgot to mention was the creditor does not care what that court orders states. Bob is still obligated to pay that mortgage until the house is sold or refinanced out of his name.

I have also received calls from past clients that thought a divorce decree protected their credit report from previous obligations. They were told this information by the attorney representing them. For example, the divorce decree stated that Bob’s wife was responsible for the car note and some credit cards. A few months later Bob get a call from a collection company that he owes them money for a car that was repossessed. To Bobs surprise even though the divorce decree stated his ex-wife was responsible for the car note; his credit report now shows 90 day late payments. Bob is now getting hounded by collections companies.

Attorney’s not giving good advice when it comes to credit has been a huge problem. I have come to the conclusion that divorce attorneys know nothing about credit laws.

So if divorce is on the horizon, anything that is awarded to your spouse, make sure that debt is out of your legal name. A good attorney will force the other party that is responsible for the obligations to get all those obligations out of your legal name. This is really the only legal way to get your credit off the hook.

Remember, a divorce decree or court order does not remove your social security number from a creditor’s database. As long as your social is attached to any particular obligation, you are responsible for that obligation regardless of what an attorney says.

Jumbo loans, which all but disappeared when the credit crunch began in 2007, are making a comeback. Not only that, jumbo mortgage rates have hit a new low of just over 5 1/4%.

Traditionally, jumbo mortgages have been offered at a considerably higher rate than conventional loans. That’s because these loans cannot be sold to Fannie Mae or Freddie Mac and must be held in the bank’s portfolio. Until recently, banks were holding off on making these loans available.

A jumbo loan is a mortgage loan in an amount that exceeds conventional conforming loan limits – which are set by Fannie Mae and Freddie Mac. That limit in 2010 is $417,000 – with a limit of $625,500 in Alaska, Hawaii, Guam, and the U.S. Virgin Islands.

Banks are being careful, even though they consider those wealthy enough to purchase high end homes to be a better credit risk. They’re demanding at least 20% as a down payment, and are putting borrowers through full documentation underwriting procedures.

This return to stricter standards also applies to homes under $417,000 – making it more difficult for buyers in every price range to obtain a home loan, and leading to speculation about the future of home ownership in America. Those who fear that home ownership will be only for the wealthy are forgetting that “average” citizens purchased homes back in the 80’s – when 20% down and strict documentation were the norm, and obtaining a 10% mortgage interest rate was cause to celebrate..

In spite of the return to rigid requirements, applications for jumbo mortgage loans are on the rise. Bank of America, for instance, reported a 10% increase in jumbo loan applications from May to June of this year.

Million dollar homes account for less than 1 ¾ % of the overall market, but sales in this category were up 77% in May 2010 over May of 2009.

Interestingly, the home-buyer tax credit appears to have been partially responsible for the bump in the number of jumbo loan applications. Buyers in this category necessarily had incomes beyond the limits to receive the credit. But because of the credit, more were able to sell their previous homes and “move up” to the jumbo loan price category.

The other reason cited for the rise in jumbo loan applications is pent-up demand for exclusive homes. After many months of being denied the opportunity to buy because jumbo loans weren’t being made, those who can afford million dollar homes are now ready to buy.

The record low interest rates are simply frosting on the cake.

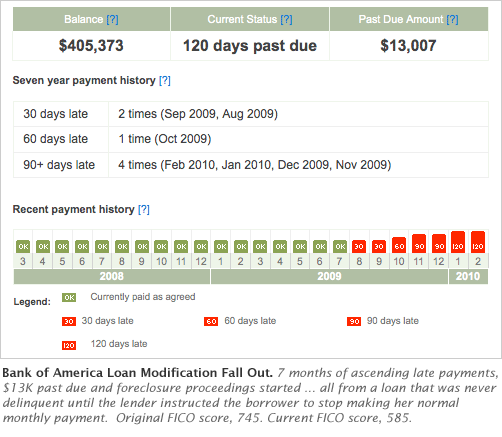

A friend called the other day to tell me that their loan modification had been rejected. After several months of paperwork and the destruction of their credit scores, the bank decided that they couldn’t afford the lower payment.

What? Until they got involved with loan modification they had been keeping up with the higher payment. They didn’t get a black mark on their credit report until the loss mitigation people instructed them to miss a payment.

They, like so many others, simply got involved in loan modification because their diminished income was making it hard. They work in real estate sales, and the market in their area has been dismal. They hoped that a lower payment for 5 years would ease the strain until the economy finally turns around.

Now, after a few months of making the modified payment, their credit report shows 30, 60, and 90 day late payments – because the amount they’d been paying was less than their original contractual agreement.

Congresswoman Jackie Speier thinks this needs to change. On July 15 she introduced a bill entitled the “Protecting Homeowner’s Credit History Act.”

This bill, HR 5743, calls for an amendment to the Fair Credit Reporting Act. If passed, it would prohibit lenders from furnishing negative loan modification information to the credit reporting agencies, and would prohibit that information from being used to compute a consumer’s credit score.

But does the fault lie with the reporting agencies?

No, it lies with the HAMP system and what they choose to report.

If loan modifications were being processed in a timely fashion – such as 30 days – there would be no impact on the borrower’s credit scores. Instead, lenders are taking as long as 9 months to process loan modifications and make their decisions.

Plus, if the bank makes a temporary agreement with the homeowner during the modification trial period, that should be the agreement on which the report is based. Paying as agreed on the temporary agreement should show on a credit report as “paid as agreed.”

Some experts say that loan modification should affect a borrower’s credit scores. Their premise is that people who modify their loans are more likely to default in the future. Of course, this hasn’t been going on long enough to have any solid research to back that presumption.

People who are determined to keep their homes do what they need to do to hang on. Therefore, many are making payments that an underwriter would say they “can’t afford.” To take it to the next step and deny modification by deciding that the homeowner who has been making a $3,000 payment without fail suddenly won’t qualify to make an $1,800 payment is nothing short of ridiculous.

Two things need to happen to the HAMP program, which has helped only about 10% of the homeowners it was supposed to have helped by last June. First, lenders must be required to process applications within 30 days Then they need to start using common sense in making their decisions.

Government regulation is ramped in our country currently. I think most Americans are under the assumption that greed caused our current turmoil. As this is partially true, the majority of the issues were stemmed from government intervention. How can regulation on such magnitude be written and approved in such a short time without repercussions? It only makes sense that businesses are built on the quality of service they provide to their customers. Logic would only show that those whom allow greed to take place will result in the failure of that particular company. The media, politicians, and government regulators would like you to believe regulation is the solution to the current economic downfall which they claim was the result of greed. Why all the sudden is greed only in one sector, the credit sector?

Here is the problem with government regulation that is really not necessary. Recently there was a bill passed that will dictate how much a mortgage originator can make on a loan. This bill is 74 FR 43232. In a nut shell this is government saying hey, we don’t want you to make what you were making anymore. You can now make only x amount of dollars per transaction.

Example of what this bills says.

The final rules, which apply to closed-end loans secured by a consumer’s dwelling, will:

Prohibit payments to the loan originator that are based on the loan’s interest rate or other terms. Compensation that is based on a fixed percentage of the loan amount is permitted.

Prohibit a mortgage broker or loan officer from receiving payments directly from a consumer while also receiving compensation from the creditor or another person.

Prohibit a mortgage broker or loan officer from “steering” a consumer to a lender offering less favorable terms in order to increase the broker’s or loan officer’s compensation.

Provide a safe harbor to facilitate compliance with the anti-steering rule.

In the past a lender could make money on the interest rate sold and fee’s charged on the good faith estimate. If the customer did not like the fees being charged, they could shop for a better deal. Does that sound so bad? Well that is what we call a free market where companies can set there own fees based on what the market will allow. Since the government has recently got involved, the free market for lending has been trampled on. This intrusion will result in the borrowers paying higher rates so the banks, mortgage brokers, and loan officers can make money.

So in a nutshell when the government interferes with the profits of a company, the cost is passed on to the consumer in some other form or fashion.

I thought this was a good video on how important it is to know what is going on with your credit.

If you have not pulled your free credit report from www.annualcreditreport.com I would recommend doing so. You cannot afford to be in the dark about your creditworthiness. You may also pull your 3 bureau credit report with our site if you have already exercised your free report with annualcreditreport.com. You can set up monitoring as well through our site.

As the U.S. economy struggles and the housing market flounders, the cost of closing a home loan continues to rise.

In fact, according to an August 16 article in the Dallas Morning News, 2010 closing costs nation-wide are up 36% from 2009. These costs are a combination of appraisal fees, title insurance, loan origination, document fees, courier fees, etc. – all of which have risen.

Bankrate.com recently conducted a survey to find the average cost of closing a loan for a good-credit buyer on a $200,000 purchase with 20% down. They found New York to have the highest costs at $5,623 – with Texas following at $4,708. At the other end of the spectrum, Arkansas was the least expensive at $3,007, followed by North Carolina at $3,255. The U.S. average was $3,741.

In Texas, where residents already pay some of the highest home insurance and property tax rates in the nation, closing costs are up 18% from their 2008 levels.

A primary reason for the jump in costs is the GFE – the mandatory good faith estimate. Lenders must now be more accurate – or they must make their estimates higher in order to avoid liability for a shortfall. Some items cannot change at all from the GFE, while others cannot vary by more than 10%.

Another reason could be the Home Valuation Code of Conduct. This regulation put a 3rd party vendor between the lender and the appraiser – and that 3rd party naturally has to be paid for its services. The result – lower fees to appraisers and higher costs to consumers.

Why have bank fees also increased? Probably because of the CARD Act and the limits it put on bank profits.

Meanwhile, as costs to buyers rise, FHA has decided there will be less risk to them if sellers are more limited in the amount they can contribute toward their buyer’s costs. Thus, the seller concession limit will likely drop from 6% to 3%.

Home buyers remain in a state of confusion as new regulations, new bank policies, and seemingly constant changes to those policies are the norm rather than the exception. Worse, every new regulation seems to add cost – but not value – to the purchase of a home.

For instance: The changes to FHA loans. When the mortgage crisis first hit, “low and no” down loans went away entirely. For a while it looked as if we would go back to the lending practices of 80’s, when you either had 20% down for a conventional loan or 5% down for a FHA loan – and you had to have a good credit score.

Now FHA is once again offering loans at 3 ½% down, and has eased the credit score requirements – but the cost of mortgage insurance has risen to help cover the risk.

Fannie Mae has also brought back 100% loans – but only if you purchase a Fannie Mae-owned home. That’s one way to get your lender-owned homes sold faster than consumer owned homes!

Meanwhile, in spite of government programs that promise to help homebuyers, banks are making it more and more difficult to obtain a home mortgage – even for people with high credit scores.

No matter where you stand in the credit card debate, “to use” or “not to use”, one thing is for certain and that is that the true cost of using credit cards and carrying a balance is very high. Many proponents of credit cards point to certain credit card benefits like rewards, convenience, fraud protection, etc. which everyone on both sides of the debate can agree are desirable things BUT is there maybe a way to have our cake and eat it too? While the goal of this article is certainly not to re-hash any of the pros and cons of credit cards let’s take a look at 3 credit card alternatives to see if we might be able to have some or all of the benefits of credit cards without the potential downsides.

#1 Rewards Debit Cards

Rewards like cash back, airline miles, and other perks seem to be one of the first things that many in the pro credit card camp will point to as the primary benefit to using a credit card. However, credit cards certainly do not have a monopoly on earning rewards. Rewards debit cards like the Perkstreet debit card offer cash back rewards just like a credit card BUT since the card is a debit card that is linked to a checking account there is no chance that the cardholder will overextend themselves on credit because there is no line of credit!

PROS

Cash back rewards

No line of credit (no chance for misusing credit)

Just as convenient to use as a credit card

CONS

Reduced fraud protection (as compared to credit cards with federal regulation protection)

#2 High Yield Checking Accounts

High yield checking accounts are a great way to not only have all of the convenience of a credit card (assuming that the high yield checking account you choose offers debit card access) while at the same time avoiding any potential misuse of credit, forcing one to save money and live within their means, and earning a relatively high rate of interest on money in the account at the same time! High yield checking accounts often have more onerous restrictions than typical checking accounts (i.e. balance requirements, spending requirements, etc.) but have interest rates that are currently averaging anywhere from 1% all the way up to close to 5%!

PROS

High interest rate on deposited funds

No line of credit (no chance for misusing credit)

Just as convenient to use as a credit card (assuming debit card access)

CONS

Reduced fraud protection (as compared to credit cards with federal regulation protection)

Restrictions and requirements for earning maximum interest rates

#3 Secured Credit Cards

Wait! I thought we were looking at credit card alternatives… Isn’t a secured credit card still a credit card? Well, kind of. There is no line of credit associated with a secured credit card as a secured credit card functions much like a debit card in that you can only use the card to spend money that you have first deposited into your account.

OK… so if a secured credit card works essentially the same as a debit card then why not just get a debit card? One major benefit to using a secured credit card is that most secured credit cards report to the 3 major credit reporting bureaus which will in turn help to improve your credit score over time.

If you already have great credit and are out for rewards, rewards, and more rewards then stick with a reward debit card or a high yield checking account because a secured credit card is not for you. However, if your credit score could use a little work then utilizing a secured credit card might just be a smart way to give your credit score a boost and help you to quality for lower mortgage rates, lower auto loan rates, better insurance rates, etc.

PROS

Ability to improve credit score over time

No line of credit (no chance for misusing credit)

All of the convenience of a credit card (and a secured credit card is still viewed as a credit card and not a debit card so much easier when trying to buy a cell phone, get a rental car, etc).

CONS

Little to no rewards

Some cards have high fees

Money deposited into account does not earn interest (similar to a regular checking account but unlike a high yield checking account)

So… What Should I Choose?

Well, there is no one choice that is best for everyone but it is always good advice to do your homework, research all of your options thoroughly, weigh the pros and cons of each type of financial product that you have available to you and then make an educated decision. Be an educated consumer and even (gasp) read the fine print for any type of financial product that you are considering before making the leap.

What do YOU Think?

What do YOU think is the best credit card alternative?

What are some of the most important features for you to have in a method of payment?

Do you have any other alternatives to using a credit card besides the 3 mentioned above?

Author Bio: Joel Ohman is a Certified Financial Planner™ and a serial entrepreneur. Some of his current projects include a website for anyone that wants to compare car insurance and a website with some nifty online calculators. Joel is new to CreditScoreQuick.com and would encourage you to check out the credit resources section of the site.

Bankruptcy is sometimes hard to avoid, especially during tough economic times. Let’s face it, nobody wants to file bankruptcy. There are two types of common bankruptcies. They are Chapter 7 and Chapter 13. Once your bankruptcy is discharged you will need to re-establish your credit score with each credit bureau.

Instructions:

1. Make sure you pay all your current bills on-time. You definitely don’t want troubles after a bankruptcy is on your credit report. Have a realistic budget and stick to your budget. If you find that you are having problems paying any debts, make payment arrangements with your creditors. Creditors will typically work with emergency circumstances. Remember your payment history accounts for 35% of your overall credit rating.

2. Get a family member to add you as an authorized user on a credit card. This will allow you to ride the coat tail of someone that has good credit. Also get a couple of secured credit cards. Secured credit cards are a great way to re-establish credit.

3. Establish at least 3 lines of good credit on your credit report. This is very important. I know that maybe credit card got you in trouble to begin with, but they are a necessary evil. With 12 to 24 months of good payment history you will see an improvement in your credit scores.

4. Get some installment loans. Installment loans are a great way to re-establish credit after a bankruptcy discharge. Typically car loans are easier to get when you have low credit scores.

5. Have savings for emergencies. Any financial adviser will recommend that you have 6 months worth of income in savings. When something happens you have some breathing room until you can resolve matters. If you don’t have any savings, then avoid all the little pleasures, like eating out, going to the movies, shopping for clothes, etc….until you have 6 months income in the bank.

Over the last 10 years FHA was providing financing to just about anyone. They also allowed you to get into a home with little or no investment. So essentially you could buy a home and actually get money back at closing. Sound crazy? Well it was going on everywhere. Now the bar for FHA credit criteria has been raised, but the damage has already been done.

During 2007 the bottom fell out of real estate and foreclosures were on the rise. FHA charges an up front Mortgage Insurance Premium (M.I.P.) and a monthly Mortgage Insurance (M.I.) to the cover the cost of these foreclosures. M.I.P. is a one time fee of 2.25% of loan amount that is financed into the note. Earlier this year the M.I.P. was 1.75, which was increased to 2.25%. They also charge .50% of your loan amount that is paid monthly. Well according to HUD they are running out of money to cover all the claims due to foreclosures with the current premiums.

So they have recently passed a bill that will increase the monthly M.I. to .80% of your loan amount and drop the M.I.P. to 1% on October 4th of this year. How does this affect you? See example Below.

We will use a home of $100,000 for an example.

Illustration from Bankrate.com

You can see how the changes will cause an increase in your monthly payment. Your payment will increase $22 bucks a month with this scenario provided on a $100,000 dollar home. So if you are in the market to buy and FHA is your route, you may want to buy before October 3rd of this year. According to Bankrate.com the new changes will take affect on October 4th.

Disclaimer: This information has been compiled and provided by CreditScoreQuick.com as an informational service to the public. While our goal is to provide information that will help consumers to manage their credit and debt, this information should not be considered legal advice. Such advice must be specific to the various circumstances of each person's situation, and the general information provided on these pages should not be used as a substitute for the advice of competent legal counsel.